Five stories that matter

⚡ 01 NVIDIA writes its first cheque into legal tech, topping up Legora’s Series D to $600M

Legora extended its Series D by $50M at a $5.6B valuation. NVentures, NVIDIA’s venture arm, joined alongside Atlassian, Airtree, Barclays and Geodesic. Per Dealroom, this is NVIDIA’s first investment in a legal-tech company. Atlassian is also new to the cap table. Both names are signal: a hyperscaler-adjacent fund and a horizontal SaaS strategic, both betting on the same vertical AI thesis on the same day.

⚡ 02 RELX agrees to acquire Doctrine, the leading French legal AI platform

LexisNexis’s parent offered to buy Doctrine, the Paris-based platform built around the French case-law and statutory corpus and used daily by lawyers in France, Italy, Germany and Spain. Terms not disclosed. The strategic logic is the same one that animated last week’s LexisNexis–Luminance alliance: the moat in legal AI is moving from the model to the data underneath it, and the incumbents are buying the data they don’t already own.

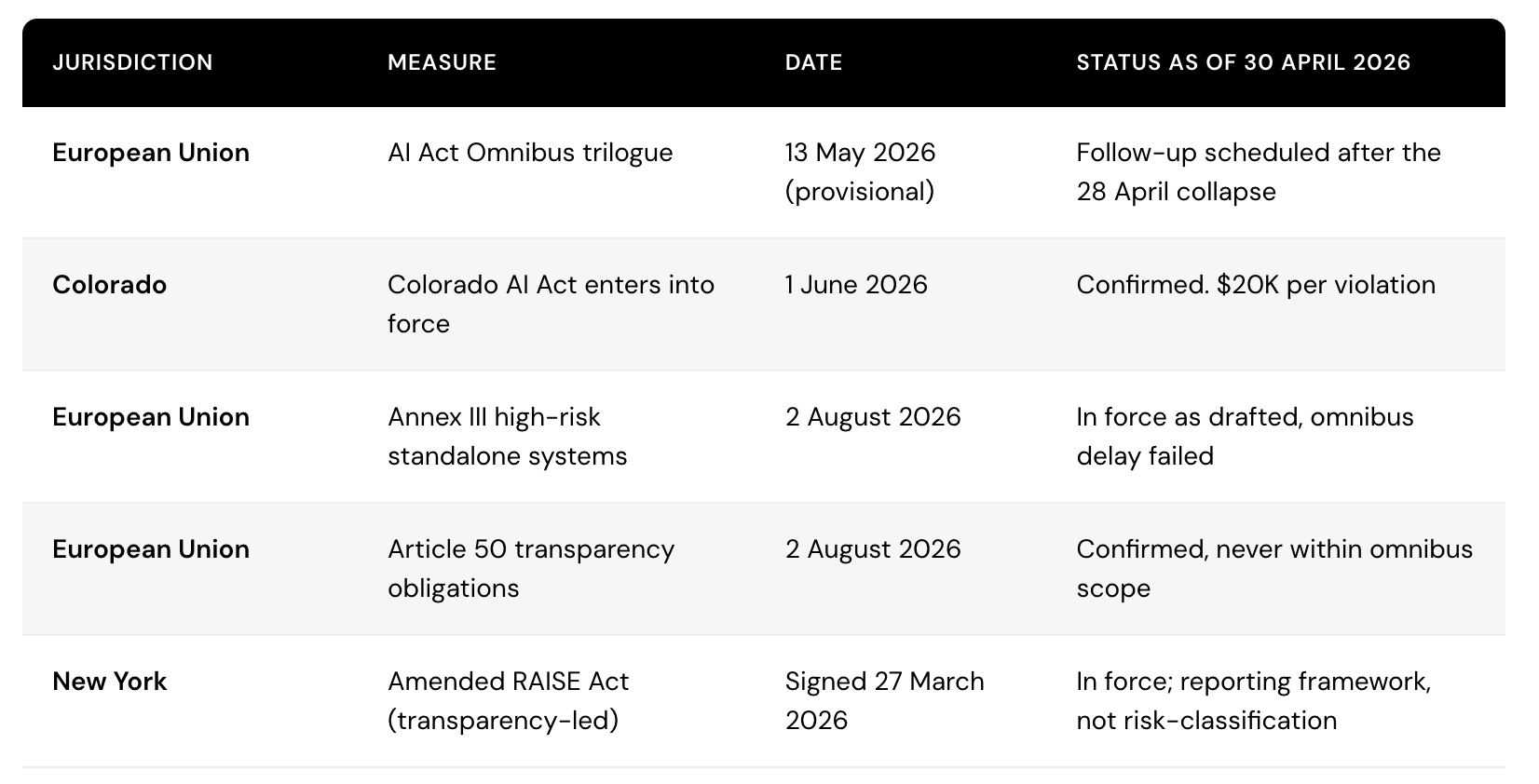

🏗 03 EU AI Act Omnibus trilogue collapses after twelve hours of negotiation

The Council and Parliament could not converge on the conformity-assessment architecture for high-risk AI in regulated products. The package would have postponed the August 2026 high-risk deadline, narrowed Annex III, and aligned AI obligations with sectoral product-safety law. None of it passed. A follow-up trilogue is provisionally targeted for around 13 May. The original AI Act timeline - 2 August 2026 - is back in force as the default planning assumption. Read IAPP’s analysis for the procedural detail.

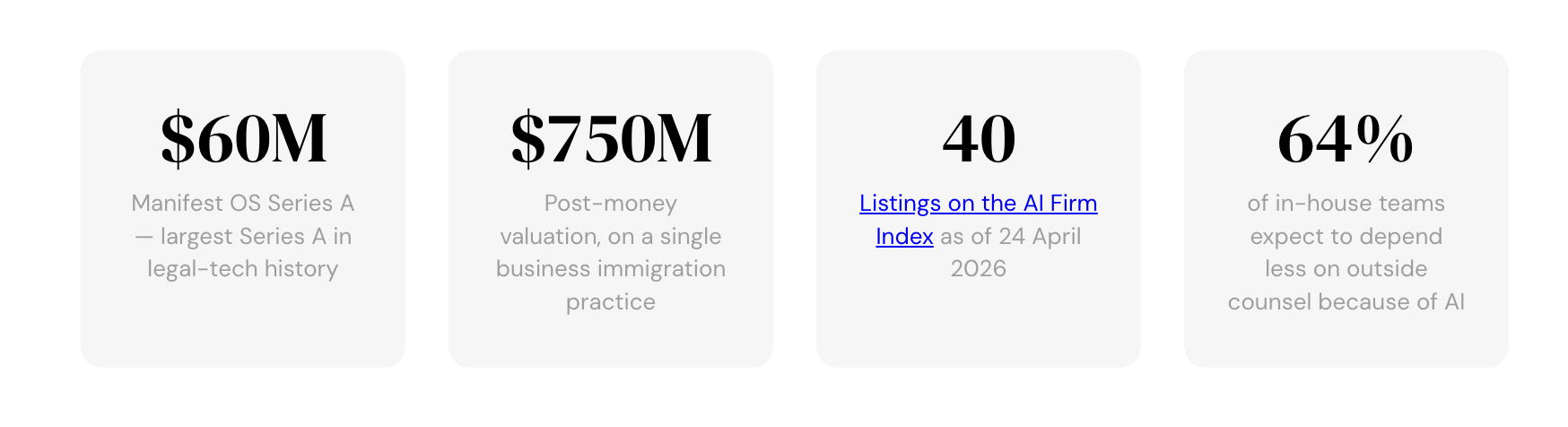

⚡ 04 Manifest OS raises $60M Series A at a $750M valuation - the largest Series A in legal-tech history

Menlo Ventures led, with Kleiner Perkins, First Round and Quiet Capital. Manifest OS is building software and centralised back-office services for a network of affiliated, AI-native law firms operating under Arizona’s ABS regime, beginning with a business immigration practice. The pitch in the company’s own words: “end the billable hour.”

⚖️ 05 A federal judge sanctions a Cherry Hill attorney for AI fabrications — for the second time

U.S. District Judge Kai N. Scott imposed a $5,000 sanction on attorney Raja Rajan in the Eastern District of Pennsylvania for filing a brief containing AI-generated hallucinations. It was Rajan’s second sanction from the same judge in three months; the first, in February, was $2,500. The pattern that’s emerging in the database is no longer one-off carelessness. It is repeat offence by the same lawyers under the same workflow.

✳️ Scroll down for The Flank View with practical insights ✳️

⚡ 01 The hyperscaler arrives in legal tech

Legora’s $50M extension is not, on its own, the interesting story. The interesting story is who wrote the cheques. NVentures is NVIDIA’s first investment into a legal-tech company. Atlassian is also on the cap table for the first time. Both arrived on the same day.

NVIDIA’s venture programme has, until now, been almost entirely focused on infrastructure layers - model providers, robotics, biotech, autonomous driving. A vertical SaaS company writing legal workflows is several rungs further up the stack than NVentures has historically gone. The signal is partly about Legora specifically - its run from $1M to $100M ARR in eighteen months is the fastest-scaling enterprise vertical AI trajectory on record - and partly about the category. NVIDIA’s portfolio is a reasonable proxy for where the firm thinks compute demand is going to grow. It is now treating legal as one of those places.

Atlassian’s investment is a different kind of signal. Atlassian sells horizontal collaboration software to engineering and IT teams. It does not sell to legal. The most plausible reading is that Atlassian is hedging into the next category of agentic, vertical workflow software - the same way Salesforce and ServiceNow have been quietly making moves in legal-adjacent categories. The shape of the bet is that the productivity gains from agentic AI in a vertical workflow are too large for a horizontal vendor to ignore.

The structural read. Two distinct kinds of strategic capital arrived on the cap table of the same legal-AI company on the same day. NVIDIA is signalling that legal is now compute-relevant. Atlassian is signalling that vertical workflow agents are now SaaS-relevant. The legal-AI category has spent the past eighteen months convincing legal-tech investors. This week is the first round in which it convinced the people upstream of legal-tech investors.

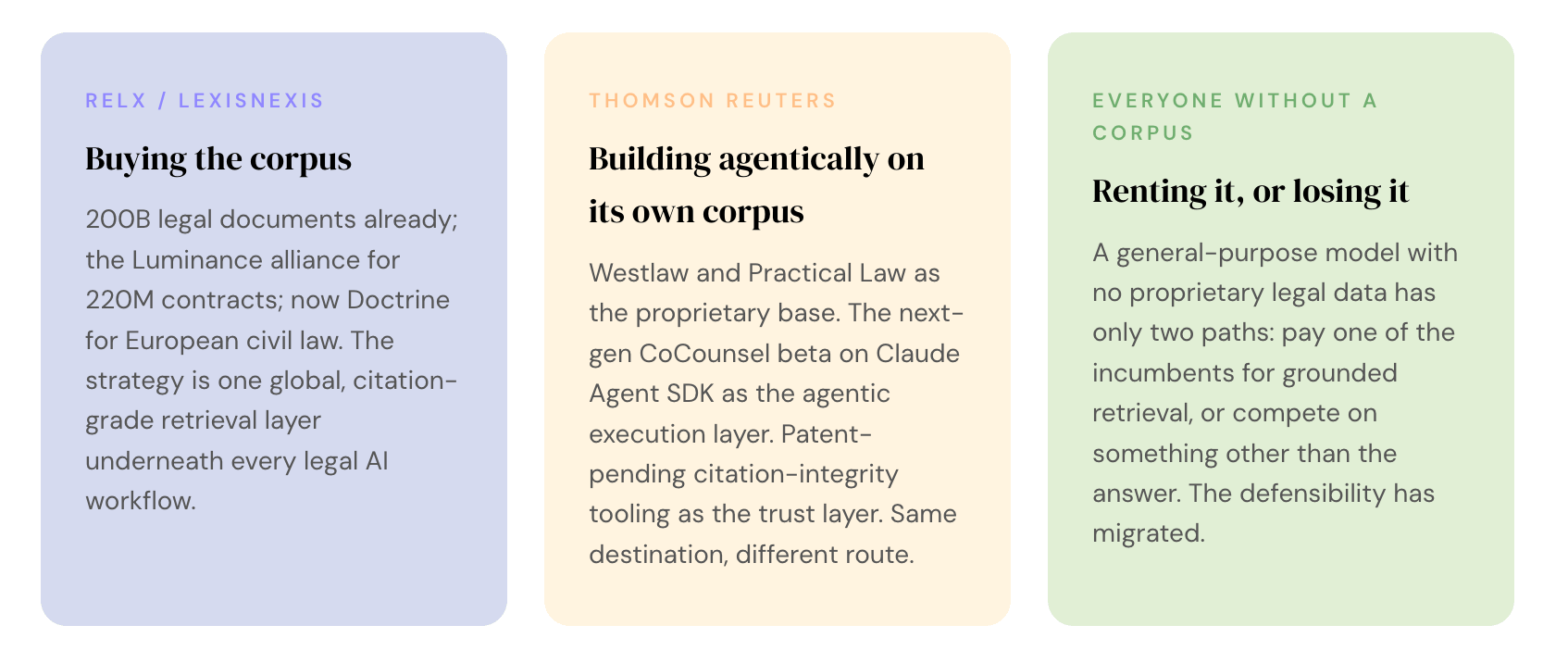

⚡ 02 RELX is buying the data it does not already own

Doctrine, founded in Paris in 2016, sits on the most complete machine-readable corpus of French case law and legislation outside the state. It is also the leading legal AI platform across France, Italy, Germany and Spain. RELX is not buying a model. It is buying a corpus and a country.

The pattern is the same one we wrote about last week with the LexisNexis–Luminance alliance. The legal-AI moat is moving from the model - which is increasingly a commodity - to the proprietary content underneath it. LexisNexis brings 200 billion legal documents in English-language jurisdictions; Luminance brings 220 million contracts; Doctrine brings the European-civil-law corpus and a working in-context assistant trained on it. The end-state architecture is a single grounded retrieval surface for a global enterprise legal team, with citations that pass courtroom and regulator scrutiny in every major jurisdiction the team operates in.

The consolidation thesis we have flagged in earlier editions is now visibly underway. Cooley’s 24 April survey of US state AI laws arrived in the same week, and reads as a parallel story on the regulatory side: many of the AI-specific state regimes that passed quickly in 2024 and 2025 are being amended, narrowed, or delayed as harmonised standards fail to materialise on schedule. Both sides of the market - the vendors and the rule-makers - are converging toward fewer, larger, more authoritative units.

The question worth asking. A general-purpose model with no proprietary legal data has only two paths left: pay one of the incumbents for grounded retrieval, or compete on something other than the answer. The defensibility has migrated. What does an enterprise legal AI procurement look like in twelve months when the only three vendors with a citation-grade corpus are RELX, Thomson Reuters and a handful of national champions the incumbents have not bought yet?

🏗 03+05 The August deadline is back, and the rulebook is not

After roughly twelve hours in the room on 28 April, the EU institutions could not agree on how the AI Act ought to interface with the existing product-safety regimes for medical devices, machinery and in-vitro diagnostics. The omnibus did not pass. The original deadline did not move.

The package that failed would have given enterprise AI deployers an extra fifteen months on standalone high-risk systems and an extra two years on AI embedded in regulated products. It also would have narrowed the scope of Annex III. The collapse means the 2 August 2026 deadline is once again the legally binding planning date - for systems that the harmonised standards needed to comply with do not yet exist for. A follow-up trilogue is provisionally targeted for around 13 May, but no one is treating that date as load-bearing.

The US picture from the same week is, if anything, more incoherent. Troutman’s 27 April state-law update tracked another cluster of proposals at various stages, and the Cooley survey two days earlier confirmed that several of the headline 2024–25 state AI regimes - including New York’s RAISE Act, materially amended on 27 March - are being narrowed, delayed, or rebuilt around transparency rather than risk-classification. California’s executive order from late March pushes toward state-procurement-only rules. The federal preemption framework, published in March, has not advanced.

What the Rajan sanction is telling us, separately

The same week, in Philadelphia, U.S. District Judge Kai N. Scott imposed a $5,000 sanction on Cherry Hill attorney Raja Rajan for filing a brief containing AI-generated hallucinations. It was the second time the same judge had sanctioned the same lawyer for the same workflow failure inside three months. The first sanction, in February, was $2,500 - the doubling is a deliberate signal to the bar.

The interesting feature is the repeat offence. Damien Charlotin’s hallucination database has crossed 1,350 globally documented cases. The volume story - already covered in earlier editions of this briefing - is established. The new pattern, visible only in the last six weeks, is that a non-trivial subset of the names in that database are appearing twice. Sanction-then-correct does not seem to be working as a behavioural intervention. The lawyers being sanctioned are in some cases the same lawyers, returning with the same workflow.

The question worth asking. The rulebook the enterprise has to plan against is fragmenting in Brussels and rebuilding in the states, with no harmonised standards arriving on schedule. Inside that vacuum, the bar’s own discipline mechanism is failing on the second pass against the same actors. If neither the regulator nor the court can change the workflow, what is left to change it?

⚡ 04 Capital is now funding the end of the billable hour, not just better tools for it

The Manifest OS round is the cleanest articulation we have seen of where the legal-AI thesis is actually pointing. It is not a tool for a law firm. It is a platform that operates law firms.

Manifest OS sits inside Arizona’s Alternative Business Structure regime - the only US jurisdiction in which non-lawyers can hold equity in a law firm. The company itself is the technology and shared services layer. The law firms - beginning with a business immigration practice trading as “Manifest Law” - are affiliated entities that run on top of it. The work is delivered at a fixed price tied to outcomes. The capital is going into more practice areas, more firms, and more centralised back-office to support them.

What Menlo, Kleiner, First Round and Quiet are funding, in other words, is a structural alternative to the billable hour, capitalised at $750 million on Series A. The closest historical parallel is Atrium - the Justin Kan project that collapsed in 2020 after burning $75M. Atrium tried to do the same thing with a much weaker AI stack, no agentic execution layer, and only a pilot ABS in Utah on the horizon. The model never had the unit economics to work. Six years later, the unit economics may have moved.

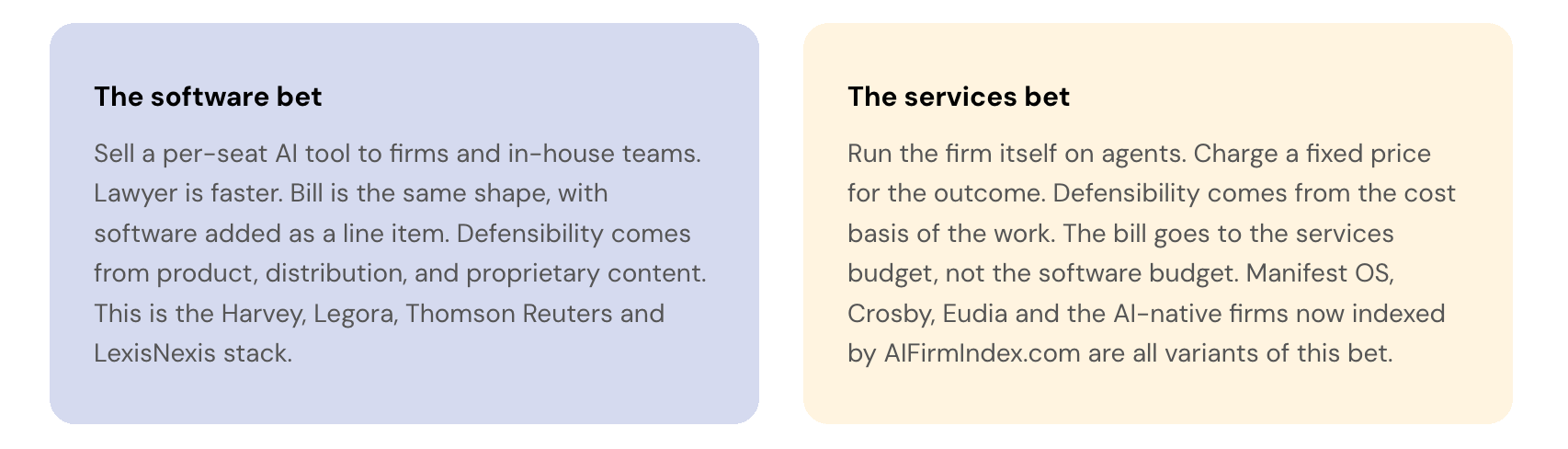

Why this round is different from a Harvey or a Legora round

The legal-AI rounds of the last twelve months - Harvey at $11B, Legora at $5.55B, now $5.6B - are bets on a software vendor with enterprise distribution. The buyer is a law firm or an in-house legal team. The product sits next to a lawyer and makes the lawyer faster. The repricing happens, if it happens, at the seat-licence level.

Manifest OS is a bet on the services line, not the software line. The buyer is a corporate counterparty looking for an immigration filing or a contract turn, and the bill they receive does not have a lawyer-hour on it at all. There is a lawyer in the loop - Arizona ABS still requires one - but the unit being priced is the outcome, not the time. The infrastructure underneath that outcome is agentic: drafting, redlining, and intake handled by software, with the lawyer supervising. Same shape as a supervised-agent service, dressed inside a law firm wrapper rather than a SaaS one.

The question worth asking. If a $60M Series A at $750M post-money is now defensible on a single immigration practice, what is the right valuation on the same model applied to commercial contracting, employment, and procurement - the categories that account for the majority of in-house spend? The legal-AI vendors raised against the software budget. Manifest OS raised against the services budget. Those are not the same number.

🧠 What this week tells us

Three of this week’s five stories are, on the surface, funding announcements. Read together, they describe a capital market that has stopped funding faster lawyers and started funding the alternative to lawyers. The other two - Doctrine and the EU collapse - explain why the budget for that alternative is now where it is.

The services budget is now the venture target. Manifest OS at $750M post-money on a single immigration practice is the cleanest data point we have that capital is now backing the law-firm replacement, not the law-firm productivity tool. Forty AI-native firms now indexed on AIFirmIndex.com. The Atrium pattern from 2020 has materially better unit economics in 2026 because the AI under the hood actually does the work.

The hyperscaler is in the room. NVentures into Legora is the first time NVIDIA has put venture capital into a legal company. Atlassian is also new on the cap table. Vertical legal AI is now a category the people upstream of legal-tech investors think they need to be present in. The implication is that the next wave of capital will not have to be educated about the market.

The moat is the corpus, not the model. RELX buying Doctrine is the third move in three weeks pointing the same way. LexisNexis–Luminance, Thomson Reuters’ fiduciary-grade CoCounsel beta, and now the European civil-law corpus all line up on one read: a general-purpose model without proprietary legal data is no longer commercially defensible at enterprise prices.

The rulebook is fragmenting, not converging. The Brussels collapse, the Cooley survey of state AI laws being rebuilt, and the Troutman tracker of new proposals all describe the same thing: more rules, narrower in scope, written faster, harmonising less. Compliance complexity is the steady state. Enterprise legal teams have to plan against a rulebook that no jurisdiction has finished writing.

The repeat sanction is the workflow problem made visible. A second sanction on the same lawyer in three months is not a training failure. It is a workflow failure that policy and discipline cannot fix on their own. The pattern matters because it isolates the variable: the lawyer kept the workflow, and the workflow kept producing the same defect.

✳️ The Flank view

The most useful frame for this week’s news is to look at where each dollar of capital actually lands inside a corporate buyer. The Harvey, Legora and Thomson Reuters rounds are bets on the software budget - the line item that pays for tools sitting next to a lawyer. The Manifest OS round, and the AI-native-firm category it now leads, is a bet on the services budget - the line item that pays for the lawyer to do the work in the first place. The services line is the larger of the two. It is also the one that has been resistant to repricing for forty years, because the work was structurally tied to the resource doing it.

Our running argument has been that the legal industry’s defining problem is structural: inexpensive work is being done by expensive resources, inside a billing model that rewards the time those resources spend, not the outcome they produce. Manifest OS is now the most explicit attempt anyone has made to attack that problem with venture capital. The implication for an enterprise legal team watching from the GC’s chair is not that the law firms will fix this. It is that the next contract for high-volume routine work - NDAs, MSAs, procurement, intake, vendor paper - will be available, this year, from a provider whose unit of price is the outcome and whose execution layer is a supervised agent. That is the conversation we have been having with customers for eighteen months. This is the week the rest of the market started asking us to have it with them.

✳️