The legal services market is not one market. It is at least three, each with a different economic engine, and I think agents will hit each one differently. The conversation tends to collapse this into a single narrative, either “AI will replace lawyers” or “AI is just a tool,” and both framings miss the more interesting structural question. Where does the economic model itself change, and where does it merely get more efficient?

capital follows different logics depending on which of the three markets it is targeting, and the consequences for the people who work in each are quite different.

This is what I find myself thinking about when I read the latest numbers. Legal tech spending at law firms surged 9.7% year on year, the fastest growth ever recorded. Legora just raised $550M at a $5.5 billion valuation to expand into the US. Harvey is reportedly raising at $11 billion. The capital flowing into this space is enormous. But capital follows different logics depending on which of the three markets it is targeting, and the consequences for the people who work in each are quite different.

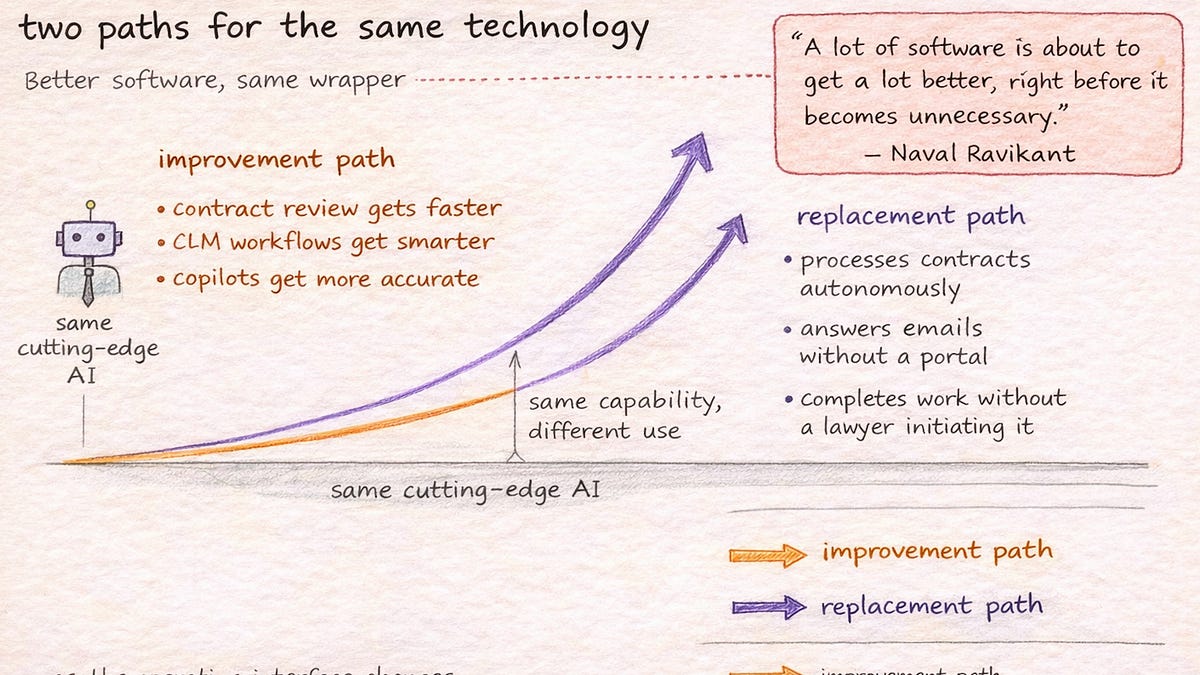

Law firms sell time. Agents compress time.

The Georgetown/Thomson Reuters State of the Legal Market report paints a picture that is worth reading carefully. Law firm profits are at record highs. Demand, however, is forecast to decline to negative 0.7% by the third quarter of this year. And AI is beginning to compress billable hours while 90% of firm revenue remains time-based.

I think the “law firms are doomed” narrative is as lazy as the “nothing will change” narrative. Large firms have survived structural shifts before.

These facts sit uncomfortably together. If your revenue model charges by the hour, and the technology you are adopting makes the hours shorter, you have a structural problem that no amount of efficiency gain resolves. Firms can raise rates, which they have been doing. They can shift toward higher-value advisory work, which they are attempting. But the base layer of legal work, the contract reviews, due diligence, document drafting, and research tasks that generate a significant portion of associate billing, is precisely the work that agents are best at compressing.

I want to be careful here, because I think the “law firms are doomed” narrative is as lazy as the “nothing will change” narrative. Large firms have survived structural shifts before. They have pricing power, client relationships, and regulatory moats that make wholesale displacement unlikely in any near-term horizon. What I think is more likely is something subtler and more destabilising: a gradual compression of the work that funds the apprenticeship model.

Consider what happens when a client deploys agents internally to handle NDA review, vendor agreement triage, and standard contract drafting. That work used to go to a law firm. Not the complex negotiation or the novel regulatory question, but the routine volume, the junior associate work that fills the base of the billing pyramid. If 20 to 30% of the matters a client sends to outside counsel are routine enough for an agent to handle, the revenue impact on the firm is direct. And the developmental impact is harder to quantify but possibly more significant: fewer junior lawyers getting trained on the foundational work that teaches them how to become senior lawyers.

The firms investing 9.7% more in legal tech are, I think, doing the right thing. But it is worth noting what they are buying. Most of the technology being adopted by firms, Harvey’s Agent Builder, Legora’s Workflows, CoCounsel’s document review, is designed to make the firm’s own lawyers more productive. The commercial logic is clear: if AI compresses the hours, make sure the hours that remain are more valuable, and make sure the firm controls the AI rather than the client. Harvey’s Shared Spaces feature, which lets firms extend their AI directly to in-house clients, is a particularly shrewd move. It keeps the client inside the firm’s ecosystem even as the nature of the work changes.

If the client can deploy their own agents, supervised by their own lawyers, running on their own playbooks, the incentive to route routine work through a law firm weakens.

But the question I keep returning to is whether this is a sustainable response or a temporary one. If the client can deploy their own agents, supervised by their own lawyers, running on their own playbooks, the incentive to route routine work through a law firm weakens. The firm’s value proposition consolidates around judgment, relationships, and specialist knowledge. Which is arguably where it should have been all along, but the revenue implications of shedding the commodity layer are real.

Service providers sell labour arbitrage. Agents eliminate the arbitrage.

The alternative legal services provider market sits at roughly $28.5 billion. The model is straightforward: hire lawyers and paralegals at lower cost than an in-house team or a law firm, apply standardised processes and some technology, and charge the client a managed fee for handling their volume work. It is a labour arbitrage business.

Scissero acquired Robin AI’s managed services division late last year after Robin’s reported insolvency … The logic of that acquisition is revealing: Scissero is buying people, not technology.

I find this the most interesting of the three segments to think about, because the economic logic of ALSPs is almost perfectly aligned with what agents do. An ALSP employs a team of 50 contract reviewers who process a client’s NDAs and vendor agreements at a fixed cost per document. An agent does the same work with no headcount, no office, no recruitment pipeline, and marginal cost that approaches zero at scale. The comparison is not abstract. It is a direct substitution.

The ALSP market is already consolidating. Scissero acquired Robin AI’s managed services division late last year after Robin’s reported insolvency, absorbing 70-plus staff and a client base that includes FTSE 100 and Fortune 500 companies. The logic of that acquisition is revealing: Scissero is buying people, not technology. They are scaling the traditional model, adding lawyers and paralegals, in a market that is beginning to make that model obsolete.

This is not to say ALSPs will disappear. The best ones are layering AI into their own operations, using agents to make their human teams more productive and their unit economics more competitive. Wordsmith’s partnership with Cognia Law is one example. But I think the structural vulnerability is clear. If the client can own the capability directly, deploying agents that sit inside their own team, run on their own playbooks, and build their own institutional knowledge over time, the case for outsourcing the same work to a third party becomes harder to make. The ALSP’s pitch has always been “we have the people you do not.” Agents change the denominator.

The transition will not be instant. Many in-house teams lack the operational maturity to deploy and supervise agents today. ALSPs that pivot to helping clients build that maturity, becoming implementation partners rather than labour providers, will probably thrive. The ones that continue to sell headcount against a market that increasingly rewards capability ownership may find themselves on the wrong side of a very rapid repricing.

In-house teams are cost centres. Agents change what capacity means.

The in-house segment is where I think the impact is most misunderstood, because the effect on headcount is almost certainly not what either the optimists or the pessimists expect.

The ACC/Everlaw survey found that 64% of in-house teams expect to reduce their reliance on outside counsel through AI. Only 7% have actually seen a reduction in total cost. I wrote about this gap in the previous article, but it is worth revisiting here in the context of headcount specifically, because I think the same dynamic applies internally.

In-house legal teams are not going to shrink. In most organisations I have looked at, the problem is not that there are too many lawyers. The problem is that there are not enough. The team is permanently understaffed relative to the volume of work the business generates. Headcount requests get delayed or rejected. Contractors are expensive and slow to onboard. The backlog grows.

This is the McKinsey model applied to legal. McKinsey did not fire 20,000 consultants and replace them with agents. They deployed 20,000 agents to do work that would have required hiring 20,000 additional people.

Agents address this by making capacity elastic rather than fixed. A team of 40 lawyers with agents handling routine contracting, triage, and Q&A has the effective capacity of a much larger team, without the proportional increase in salary cost. The headcount does not go down. The backlog does. The lawyers’ time shifts from processing NDAs to supervising agent output and doing the strategic, novel, high-judgment work that only they can do.

This is the McKinsey model applied to legal. McKinsey did not fire 20,000 consultants and replace them with agents. They deployed 20,000 agents to do work that would have required hiring 20,000 additional people. The existing workforce was redirected, not displaced.

I think there is a version of this that plays out differently at the margins, particularly for teams that are currently overstaffed relative to their actual workload, or for organisations where the work is genuinely and entirely routine. But for the typical enterprise in-house team, the pressure that agents relieve is the capacity constraint, not the headcount line. GCs are not looking to fire their third-year contracts lawyer. They are looking to stop that lawyer spending 60% of their week on NDA review so they can focus on the procurement restructuring that has been sitting in the “when I have time” pile for three months.

The more consequential headcount effect, if I had to guess, is on the types of roles that grow. Legal operations, the people who configure agents, build playbooks, design supervision workflows, and measure agent performance, becomes a more critical function. The paralegal role evolves from “do the work” to “check the work.” And the junior lawyer development path, as in law firms, faces a genuine question: if agents handle the routine work that used to train juniors, how do you build the next generation of senior lawyers?

What this means taken together

The impact of agents across these three segments is not uniform, and I think treating it as a single story leads to bad predictions.

Law firms face a revenue model challenge. The work that funds the pyramid is the work most susceptible to automation. Firms that adapt their commercial model and move up the value chain will be fine. Firms that rely on volume billing for routine work will lose that revenue to clients who bring the capability in-house.

In-house teams face the most interesting challenge, which is less about headcount and more about operating model. Agents do not replace the legal team. They change what the legal team does.

ALSPs face an existential question about their core value proposition. If the client can own the capability, the case for outsourcing the labour weakens dramatically. The survivors will be those who pivot from “we do the work for you” to “we help you build the machine that does the work.”

In-house teams face the most interesting challenge, which is less about headcount and more about operating model. Agents do not replace the legal team. They change what the legal team does. The capacity constraint loosens, the backlog shrinks, the business gets faster service, and the lawyers do different work. Whether that transition is smooth or chaotic depends almost entirely on whether the supervision and governance model is trustworthy enough for the GC to actually let go of the routine work.

None of this is settled. Suleyman suggested earlier this year that most legal tasks would be fully automated within 12 to 18 months. Amodei tracks current AI usage at 60% augmentation and 40% automation, with the automation share growing. Forrester predicts that 25% of planned AI spend will be deferred into 2027 due to ROI concerns. These predictions are not easily reconciled, and I think anyone who claims to know exactly how this plays out is selling something.

What I find useful is thinking about it market by market, economic model by economic model. The technology is the same. The impact is not.